Introduction

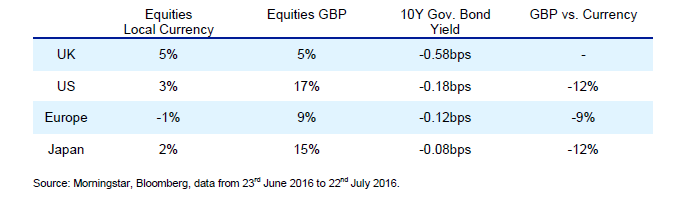

It is now one month since the 23 June EU Referendum, and few could have anticipated the positive tone to markets and surprisingly buoyant reaction to the Brexit result. Since 23 June, equity markets have rallied strongly while bond yields have fallen further, and the Sterling is still trading at an all-time low versus major currencies.

Returns since before the UK referendum:

The positive tone can be explained by a number of factors:

- Investor relief at seeing definitive leadership in the UK. Prime Minister May is seen to be pursuing a judicious review plan for Brexit as opposed to helter-skelter invocation of Treaty 50.

- Central Banks have signalled their willingness to remain accommodative in the face of any significant slowdown or systemic event, with both the Bank of England and ECB promising further support if needed.

- Elsewhere in the world, US & China have announced economic numbers which signal a stronger tone to the second quarter. Investors for the moment believe these economies to be largely insulated from events in Europe.

- The US market has hit an all-time high, buoying sentiment elsewhere in the world.

When counterbalancing these positive ‘relief’ factors, there are still some worrisome signs.

- Geopolitical events remain at the fore with weekly terrorist incidents providing an unnerving backdrop to global stability.

- Bank stocks remain under pressure across Europe, with large bank bail-outs in Italy and weakness in European bank shares a concern.

- Economic growth numbers in Europe and Japan remain weak, despite substantial liquidity injections through bond buying and negative interest rate policies in force.

- UK PMI numbers (an indicator of the health of the manufacturing sector) have shown a decisive downturn in the UK, with the headline service sector PMI falling to 47.4 (below 50 indicates slowing activity), the lowest level since 2009.

- Second-quarter earnings have kicked off with mixed results from across the globe.

Against this backcloth, investors remain watchful, feeling that there are still ample risks in the world that could derail the current rally. This has been a characteristic pattern of financial markets in 2016 – surprising market rallies following significant market declines, while bond yields continue their relentless move lower.

High volatility has boosted “safe” and income assets

Heightened volatility and the decline in bond yields have led to an enormous appetite for income and safety.

Two interesting statistics are worth noting:

- So far this year, the percentage of days when the US intra-day volatility has been greater than 2% has been close to 15% versus an average of 4% for the last 3 years. In the UK, that number is even higher.

- The yield on ten-year gilts is below the previous low recorded in 1897 and the lowest level since Bank of England records started in 1703. Today, over a third of the $25 trillion in global government bonds is yielding a negative rate of return.

As a result, stocks that look like bonds have led the rally across equity markets year to date. In the US, the telecommunications index is up 22%, utilities are up 21% and energy (because of it’s higher than market yield and the bounce in oil prices) is up 14%. Yields are close to 4% across these sectors. This pattern has been mirrored in other global markets, with utilities, staples and telecommunications up close to 10% in other developed markets excluding the US.

Is “safety” expensive?

- We believe that “safe” and high yielding stocks are now expensive, trading at an average premium of 30% to the market (see footnote). Normally, these stocks trade at anywhere between a 10-20% discount. “Safe” companies are those that offer dividend income but little earnings growth, or income stocks with high yields (such as in the energy sector) but with inherent cyclicality and risk in the underlying business.

- We believe that “safe” stocks, in particular utilities and telecommunications shares may be at significant risk as investors rotate from income sectors on rich valuations to embrace quality growth. (They also tend to be hurt when interest rates rise.)

From monetary to fiscal stimulus

What could be the catalyst for this rotation? If policy makers significantly embrace stimulative fiscal policy measures, as is expected by some, this would have a meaningfully positive impact on the outlook for growth.

Investors perceive that the monetary policy toolkit is nearing exhaustion, and negative interest rates in Europe and Japan have yet to have the desired impact on growth. As a result, the policy narrative seems to be changing. Fiscal policy is now becoming more widely discussed as a stimulus tool, and the change in policy is coinciding with political “regime shifts’:

- The EU referendum and new Prime Minister has brought an end to Osborne’s austerity, and the objective of a balanced budget for 2020.

- Japan looks close to announcing a substantial fiscal stimulus package.

- In the US, both Trump and Clinton stand for increases in infrastructure spend, potential tax amnesty for US companies to repatriate cash and reform of the tax code; with Trump calling for a lowering of the corporate tax rate from 35% to 15%.

- Xi Jinxing has implemented significant fiscal stimulus in China; many speculate that that is all part and parcel of stabilising growth at the 6% mark while cementing his leadership position for the upcoming 19th Communist Party Congress (end 2017).

Outlook

If any of these early indications of more expansionary fiscal policy come to pass, this will support portfolios with a “quality growth” bias. Interestingly, since the 24 June rally , there has been a discernible rotation in sector leadership with the perceived ‘safer’ telecom, utility and income and energy sectors underperforming other sectors (such as technology, healthcare and industrials).

It is too early to say whether this shift signals a more substantial trend reversal, but we believe it still makes sense to favour compares with quality growth, strong balance sheets, good cash flows and sustainable business franchises, which – in addition – continue to deliver earnings growth.

Given that valuation, expansion has been a significant contribution to total return, and valuations are rich as a result, there is lower scope for this to continue. Companies must now deliver earnings growth to justify further increases in valuation. In a low growth environment in which equity valuations are far from cheap, we believe investors will continue to pay for persistent and sustainable earnings.

Footnote: Source: www.bernstein.com “Keep Calm and Carry On” 2016 First Half Client Review. 30th June 2016, Bloomberg, CRSP, FactSet, MSCI, and AB. Past performance is not a reliable indicator of future returns. Safe stocks defined as the lowest quintile of monthly beta within the AB US Large Cap universe of stocks. Premium/discount is versus the universe average

Nancy Curtin

Email: [email protected]

Tel: +44 (0) 800 588 4064

Appointed in 2010, Nancy oversees a successful, award winning team of 55 investment professionals with a highly disciplined investment process.

Nancy has over 20 years’ experience including Managing Partner, Fortune, where she ran an alternatives investment business, Schroders where she was Head of Global Investments for its $20bn Global Mutual Fund businesses and Barings where she was Head of Emerging Markets and served in a range of global asset allocation roles. Nancy holds a bachelor’s degree in political science, summa cum laude, from Princeton University and an MBA from Harvard Business School.