On 17 September 2015, the Court of Justice of the European Union (‘CJEU’) rendered its decision in the case F.E. Familienprivatstiftung Eisenstadt (C-589/13) concerning the Austrian system of interim taxation of national private foundations in the case of profit allocations made to non-resident beneficiaries. The CJEU held that the unfavorable treatment of private foundations which make profit allocations to non-resident beneficiaries as compared to those making profit allocations to local beneficiaries infringes the free movement of capital.

The Austrian system of interim taxation

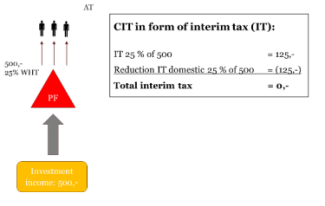

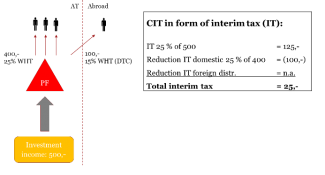

In the given case an Austrian private foundation generated capital gains which fell under the Austrian system of ‘interim taxation’. Under this taxation scheme certain profit items (i.e. certain capital gains and income from the disposal of private real estate) of a private foundation are subject to an interim tax at a rate of 25 % (corporate income tax). Before the introduction of the interim tax these profit items remained untaxed at the level of the private foundation and only the profit allocations to beneficiaries made out of this income were taxed with WHT at a rate of 25%. That mechanism allowed private foundations to reinvest profits from capital investments without consideration of any tax reductions which led to higher investment income as long as no profit allocations were made (‘snowball-effect’). However, this beneficial tax treatment – due to political reasons – had to be limited which resulted in the implementation of an interim tax. Since the interim tax should not lead to a higher overall tax burden on these profit items than under the old system (overall 25% tax burden), the base of the interim tax was reduced in so far as any profit allocations were made to beneficiaries in the same assessment period, provided the profit allocations – which are in principle subject to WHT – were not fully or partly exempted on the basis of a DTC (regularly fulfilled in case of domestic beneficiaries). If profit allocations are made in the following years for which WHT has been withheld, interim tax will be credited (in the amount of 25% of the profit allocations). Upon termination of the private foundation all interim tax not credited so far, will be refunded then.

| Scenario with foreign beneficiaries: | Scenario without foreign beneficiaries: |

|

|

The facts of the case

In the case at hand an Austrian private foundation made profit allocations to beneficiaries resident in Belgium and Germany which requested relief from the WHT deducted from their profit allocations based on the applicable DTC’s. Consequently, the Austrian tax authorities denied the corresponding reduction of the profit subject to interim tax at the level of the private foundation in the same period. The private foundation appealed before the Federal Fiscal Court (Austrian Tax Court of 2nd Instance) against this decision. However, the Federal Fiscal Court upheld the decision of the tax authorities by stating that exemption from WHT was granted in respect of the profit allocations on the basis of the DTCs, which meant that these profit allocations could not be deducted from the taxable amount of the interim tax. In a next step, the private foundation appealed against the decision of the Federal Fiscal Court before the Austrian Administrative High Court (VwGH). The Administrative High Court held it likely that the unfavorable treatment of private foundations, which arises only in the case of profit allocations to foreign beneficiaries but not in the case of profit allocations to domestic beneficiaries constitutes a restriction of the free movement of capital and referred the following question to the CJEU for a preliminary ruling: ‘Is Article 56 EC to be interpreted as precluding a system for the taxation of capital gains and income from the disposal of holdings of an Austrian private foundation in the case where that system provides for a tax charge to be imposed on the foundation in the form of an ‘interim tax’ in order to ensure single national taxation only in the case where, on the basis of a double taxation convention, the recipient of [profit allocations] from the private foundation is exempt from capital gains tax which in principle is chargeable on [profit allocations].’

The CJEU’s decision

According to the CJEU, profit allocations made by private foundations fall under the provisions of the Treaty on the movement of capital. Such profit allocations can be compared with gifts and therefore the application of Art 63 TFEU can be derived from the judgements in Persche[1] and Mattner[2]. Both the initial contribution of the assets to the private foundation by the founder as well as the subsequent payments made from profits generated by those assets to the beneficiaries fall within the concept of ‘movement of capital’ within the meaning of Art 63 para 1 TFEU.[3]

With regard to a possible infringement of that fundamental freedom the CJEU first argues that the different treatment of Austrian private foundations in their right to an immediate reduction of the interim tax base (depending on whether the beneficiaries of the profit allocation are or are not subject to Austrian WHT) forms – due to the associated liquidity disadvantage – a restriction of the free movement of capital. Although profit allocations for which such a right to immediate reduction or immediate reimbursement is excluded can also include profit allocations to beneficiaries residing in Austria where those beneficiaries are exempted from WHT, they cover in particular profit allocations made to non-resident beneficiaries in so far as under Art 21 DTC such profit allocations are not taxable in Austria since they are subject to the exclusive powers of taxation of the State of residence of the beneficiary.[4]

The CJEU concluded that the making of profit allocations by private foundations to resident beneficiaries is a situation objectively comparable to that where the same private foundations make profit allocations to beneficiaries residing in another Member State. Since Austria renounced the exercise of its powers of taxation over profit allocations to persons residing in other Member States, it cannot invoke a difference in the objective situation between resident private foundations which make profit allocations to domestic and those which make profit allocations to foreign beneficiaries in order to subject private foundations making profit allocations to the latter to a specific tax on the ground that those beneficiaries are not subject to its tax jurisdiction.[5]

The difference in treatment cannot be justified by an overriding reason in the public interest. As Austria, via the conclusion of DTC, has abandoned its powers of taxation on profit allocations to persons residing in other Member States, Austria cannot refer to a balanced allocation of powers of taxation in order to levy a specific tax on foundations that make profit allocations to such persons on the basis that those persons are not subject to its tax jurisdiction.[6]

The Court then went further to state that a ‘principle of single taxation’ has never been accepted as a distinct justification. According to settled case law any advantage resulting from the low taxation to which a subsidiary is subject cannot by itself authorise another Member State to offset that advantage by less favourable tax treatment of the parent company.[7] These considerations also apply to the case at hand, concerning a difference in tax treatment of private foundations according to whether the profit allocations they have made lead to their beneficiaries being taxed in Austria.

The restriction neither can be justified by the need to safeguard the coherency of the national tax regime. The coherency argument requires a direct link to be established between the tax advantage concerned and the offsetting of that advantage by a particular tax. According to the CJEU no such a direct link exists in the present case because of two reasons. First, the benefit of the reduction of the interim tax and the taxation of the beneficiaries concern different taxpayers. Secondly, whereas the tax advantage of the foreign beneficiary consists in a permanent exemption from the WHT, a private foundation suffers only a temporary disadvantage due to the interim tax. This is because all interim tax (insofar not credited till then) will be refunded upon termination of the private foundation.

Conclusion

This decision of the CJEU makes clear that the Austrian system of interim taxation, which refuses the right to deduct WHT-exempt profit allocations to foreign beneficiaries from the taxable basis of the interim tax, is not in line with EU law. Profit allocations of Austrian private foundations made to domestic and foreign beneficiaries should lead to a corresponding reduction of interim tax, irrespective of any tax treaty benefit applied to the profit allocations. Since the free movement of capital also applies to third country situations profit allocations to beneficiaries residing in countries outside the EU should qualify for a corresponding reduction of interim tax as well.

Way forward

Under a bill issued on 9 December 2015 the system of interim taxation was modified in order to address the CJEU judgement in F.E. Privatstiftung Eisenstadt. The new system came into force on 1 January 2016. Under the new system profit allocations to foreign beneficiaries should lead to a reduction from interim tax insofar as the profit allocations are definitely charged with Austrian WHT. Profit allocations that are only partly exempt from WHT tax, would then partly be recognized for the reduction from interim tax. Under the old system of interim taxation a partial reduction from WHT led to a full denial of reduction from interim tax.

In the event of termination of the private foundation it is now foreseen that not all interim tax will be refunded anymore, but also only to the extent (final) profit allocations are definitely charged with WHT. This amendment could even lead to situations were private foundations with foreign beneficiaries are tax even worse under the new system as compared to the old system.

As under the new bill a private foundation with foreign beneficiaries would still be treated less favorably than one with domestic beneficiaries also the new bill seems to violate EU law.

As already described above the justification of the old system of interim taxation based on the coherency of the Austrian tax system failed because of two reasons: (a) the benefit of the reduction of the interim tax and the taxation of the beneficiaries concern different taxpayers and (b) whereas the tax advantage of the foreign beneficiary consists in a permanent exemption from the WHT, a private foundation suffers only a temporary disadvantage due to the interim tax. By the new system of interim taxation (i.e. refund of interim tax upon termination of the private foundation only to the extent (final) profit allocations are definitely charged with WHT) only point (b) will be taken account of. However in its judgement F.E. Familienprivatstiftung Eisenstadt, the CJEU explicitly states the justification based on the coherency of the national tax system, fails ‘for several reasons’.[8] Therefore point (a) still prevents a justification of the new system of interim tax on the basis of the coherency argument.

To sum up the CJEU in its judgement F.E. Familienprivatstiftung Eisenstadt concluded that profit allocations to foreign beneficiaries should always lead to a full corresponding reduction of interim tax, irrespective of any DTC exemption. The Austrian legislator should therefore re-implement the system of interim taxation in a way that it does not differentiate between WHT-exemption anymore. For now it seems highly questionable whether the CJEU would accept the new system which came into force beginning of 2016. Therefore, Austrian private foundations with foreign beneficiaries which are subjected to significant interim tax and do not benefit from a reduction of it due to the regulation above should analyse whether it makes sense to challenge the Austrian regulation by referring to EU law.

[1] EU:C:2009:33 (Persche), para 27.

[2] EU:C:2010:216 (Mattner), para 20.

[3] EU:C:2015:612 (F.E. Familienprivatstiftung Eisenstadt), para 39.

[4] EU:C:2015:612 (F.E. Familienprivatstiftung Eisenstadt), para 43.

[5] EU:C:2015:612 (F.E. Familienprivatstiftung Eisenstadt), para 64.

[6] EU:C:2015:612 (F.E. Familienprivatstiftung Eisenstadt), para 71.

[7] EU:C:2015:612 (F.E. Familienprivatstiftung Eisenstadt), para 76.

[8] EU:C:2015:612 (F.E. Familienprivatstiftung Eisenstadt), para 82.