In connection with its ambition to capture and store up to 10Mt of CO2 per year by 2030, the UK government is looking to identify at least two carbon capture, usage, and storage (CCUS) clusters suited to deployment in the mid-2020s as part of its Cluster Sequencing Process.

The intention is to support the deployment of CCUS projects at a number of industrial clusters, with the potential for these clusters to be expanded into a UK carbon network as users connect to the shared transport and storage (T&S) infrastructure.

The six largest industrial clusters by the level of CO2 emissions are at Humberside, South Wales, Merseyside, Grangemouth, Southampton, and Teeside.

These account for a significant proportion of the UK’s industrial CO2 emissions and are considered to offer the most potential in terms of shared CCUS infrastructure.

CCUS Business Models

The UK government published an update to its CCUS business models in May 2021. It is through these business models that the UK government seeks to support the deployment of CCUS projects.

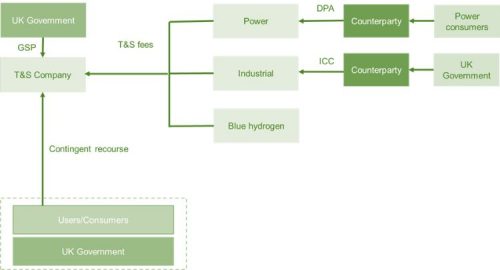

The cost of the shared T&S infrastructure is passed through to connecting carbon capture projects by way of a regulated T&S fee. These projects in turn benefit from support under Dispatchable Power Agreements and Industrial Carbon Capture Contracts.

The UK government is also looking at a business model to support “blue” hydrogen production at CCUS clusters. The intention is for shared T&S infrastructure to have sufficient capacity to enable the expansion of the CCUS cluster.

T&S Regulatory Investment Business Model (TRI Model)

The T&S company is responsible for the development, construction, financing, operation, maintenance, expansion, and decommissioning of the T&S infrastructure.

The UK government’s proposed TRI Model involves a licence being granted to the T&S company pursuant to which it receives an “allowed revenue” by charging users a regulated T&S fee to have their captured CO2 transported and stored.

The UK government is also considering incentives linked to availability, leakage rates, and connection of additional users, as well as reopeners for one-off material changes in expenditure outside the control of the T&S company. A regulator will be responsible for administering the licence and monitoring the performance of the T&S company.

It is recognised that the T&S infrastructure may be underutilised until more carbon capture projects are completed and connected to the shared T&S infrastructure, resulting in the T&S company collecting less than its allowed revenue in T&S fees.

The UK government is proposing to include mitigating measures in the TRI Model such as shaping the allowed revenue profile to align with expected utilisation build-up and providing for allowed revenue to be deferred and “rolled up” if connecting carbon capture projects are delayed.

The UK government also intends to make a contingent mechanism available to protect the T&S company’s revenues and a Government Support Package (GSP) to protect against specific high impact low probability risks.

Industrial Carbon Capture Contracts (ICC Contracts)

It is intended that CO2 emitters in sectors such as chemicals, refining, steel, and cement will invest in industrial carbon capture and connect to the shared T&S infrastructure.

In order to incentivise investment in industrial carbon capture, the UK government proposes to grant contracts that provide the CO2 emitter with a payment per tonne of captured CO2 to cover operational costs, T&S fees, and repayment of capital with a rate of return. The UK government is also looking at providing other support such as capital grants.

Dispatchable Power Agreements (DPAs)

The UK government intends to support the deployment of dispatchable power stations with carbon capture through contracts based on the contracts for difference (CfDs) used for renewables.

The proposed DPA provides availability payments for revenue certainty and variable payments to ensure that power stations with carbon capture dispatch ahead of unabated power stations by accounting for the additional costs associated with carbon capture.

It is through the DPA that the investor recovers the cost of T&S fees and capital invested in carbon capture, together with a rate of return.

Interdependency

T&S infrastructure investment is dependent on carbon capture projects being completed and connected. In turn, carbon capture projects are dependent on the T&S infrastructure being available.

It is through the expansion of the CCUS cluster that the T&S infrastructure can be used efficiently and costs per tonne of CO2 reduced.

Pipeline capacity and connection arrangements will be important when it comes to expanding the CCUS cluster and making full use of the shared T&S infrastructure.

The UK government is looking to mitigate risks associated with interdependency through mitigating measures and a contingent mechanism (see above), but investment in T&S infrastructure and carbon capture projects will necessarily take into account the other projects making up the CCUS cluster and potential expansion of the CCUS cluster. Individual projects are not able to stand on their own, notwithstanding that mitigating measures and a contingent mechanism may be used to plug gaps.

It is through the Cluster Sequencing Process that the UK government aims to support the efficient deployment of CCUS. Those projects which form part of a “Track 1” cluster will have the first opportunity to be considered for support.

The UK government announced on 30 July 2021 that five clusters met the eligibility criteria set out in its Cluster Sequencing Process.

These clusters are referred to as DelpHYnus, HyNet, the East Coast Cluster (ECC), the V Net Zero (VNZ) Cluster, and the Scottish Cluster. The UK government expects to announce “Track 1” clusters from 25 October 2021.

Carbon Pricing and Carbon Border Adjustment

In practice, policies to reduce CO2 emissions and incentivise CCUS will not work if carbon-intensive industry relocates to countries with less stringent climate regulations (or where there are stringent climate regulations but these are not enforced effectively).

There is no point in reducing CO2 emissions in the UK by shifting emissions to other countries. There needs to be a reduction in global CO2 emissions.

The proposed business models effectively pass the cost associated with CCUS through to UK taxpayers and consumers, but what happens after this support falls away?

If operational costs and T&S fees are no longer supported by UK taxpayers and consumers, continuing to capture carbon and connect to the T&S infrastructure will represent an additional cost for CO2 emitters.

This in turn has consequences for the shared T&S infrastructure.

UK carbon pricing and activism on the part of shareholders and consumers provides an incentive for CO2 emitters to continue to capture carbon and connect to the T&S infrastructure, but there is a question as to whether this will be sufficient if countries with less stringent climate regulations offer a cheaper alternative.

This is not just an issue for the UK and there has been a push for coordinated action across countries to reduce global CO2 emissions.

It is important to look at the global supply chain and ensure that CO2 emissions are not just shifted to countries where there are less stringent climate regulations.

If global supply chains are used to import materials or components from such countries at a lower cost we will just be shifting CO2 emissions, so measures such as ESG reporting will be needed to improve standards across the global supply chain.

ESG reporting offers to provide transparency with respect to the carbon footprint of a company’s global supply chain, enabling consumers and investors to distinguish between businesses that shift CO2 emissions to other countries and those that do not.

The FCA is currently consulting on extending climate-related disclosure requirements to more listed companies and institutional investors are voting against management at companies failing to address environmental issues.

However, so long as businesses can reduce costs by importing materials or components from countries with less stringent climate regulations there will be an issue with CO2 emissions being shifted to such countries.

In order to address this, countries have been looking at carbon border adjustments whereby imports from countries with less stringent climate regulations will face an additional charge to level the playing field.

If the UK government were to introduce a carbon border adjustment, it would be able to impose a higher cost on CO2 emitters without shifting CO2 emissions to other countries.

This would incentivise the expansion of the CCUS clusters without direct support from UK taxpayers and consumers. UK exporters will still be at a disadvantage in international markets when competing against companies that do not have to reduce their CO2 emissions, but coordination across countries in terms of carbon border adjustments will mitigate this.

The cost associated with reducing CO2 emissions still lands with the consumer in the form of higher prices, but CO2 emitters and global supply chains would be incentivised through the competitive market to minimise the cost of reducing their CO2 emissions.

This could, in turn, result in opportunities for CCUS clusters that are able to capture, transport, and store CO2 at a relatively low cost (i.e. companies may invest in, or source materials or components from, plants or production facilities at a CCUS cluster in the UK rather than those in countries with less stringent climate regulations if the carbon border adjustment outweighs the cost of carbon capture, transport, and storage at the CCUS cluster). This would have a real impact on global CO2 emissions.

Investment in Carbon Capture

There is a move away from carbon-intensive industries to renewables and CCUS as banks, private equity firms and other financial investors look at aligning their lending and investment portfolios with net-zero emissions.

In particular, some 53 banks from 27 countries representing almost a quarter of global banking assets have committed to aligning their lending and investment portfolios with net-zero emissions by 2050 as part of the Net-Zero Banking Alliance and there is an initiative to develop a standard for banks to measure and report on their social and environmental impact.

There has been a lot of interest in CCUS and the expectation is that significant financing will be available to support projects which are aligned with reducing CO2 emissions. Industrial companies and oil majors are also looking at investment in CCUS.

Conclusion

The fact that the UK government’s proposed business models are based on existing regulated asset base models and contracts for difference is positive for investors.

The decision to invest in T&S infrastructure or to provide financing will rest on confidence in the revenue that will be allowed under the TRI Model, the status of the different projects making up the CCUS cluster, and the extent to which mitigating measures and contingent mechanisms will plug any gaps that may arise.

CO2 emitters and other investors in carbon capture will look at that the ICC Contract and whether it covers operational costs, T&S fees, and repayment of capital together with a rate of return.

The term of the ICC Contract will be important and, to the extent that the carbon capture equipment is still operational after the ICC Contract falls away, CO2 emitters and investors will be looking at carbon pricing and potential measures such as carbon border adjustments to ensure that there is long term demand for CCUS without relying on direct support from the UK government and consumers.

In the long term, these measures could lead to opportunities for CCUS clusters that are able to capture, transport, and store CO2 at a relatively low cost.