Until March 2013, the private placement of alternative investment funds was quasi-unregulated in Switzerland. Any type of investors could be solicited by any type of funds as long as the solicitation was not falling into the category of “public placement”.

A number of distribution scandals affecting retail investors during the past decade pushed the European Commission and the Swiss legislator to introduce new regulations with a view to provide better protection to investors.

Europe has heavily regulated the distribution of alternative funds through the AIFMD. The Swiss Parliament decided to adopt a pragmatic and lighter approach that would in essence preserve the former private placement regime but only for sophisticated investors. In March 2013, the modification of the Swiss Collective Investment Schemes Act (CISA) and its implementing ordinance, the Collective Investment Schemes Ordinance (CISO) entered into force.

- The new Swiss regulation in a nutshell

The notion of private placement has been replaced in the new law by the notion of “distribution”. Any type of activity or action whose object or purpose is to generate investment in a collective investment schemes is deemed to be distribution.

In essence, the new Swiss regulation regarding the distribution of foreign collective investment schemes had the effect to create three categories of investors : 1) the non-qualified investors; 2) the non-regulated qualified investors and 3) the regulated qualified investors. Today, non-qualified investors can only be solicited by Swiss funds and by European UCITS duly registered and authorised by FINMA (the Swiss regulator). The solicitation of non-qualified investors by alternative funds is now strictly forbidden and liable to criminal penalty. On the other hand, the solicitation in Switzerland of qualified investors by alternative funds has been left wide-open, with only minimal constraints for the fund provider but some requirements for the fund distributor (the entity that will solicit qualified investors in Switzerland).

The solicitation of regulated qualified investors (mainly banks and insurance companies) is completely free and does not require any action, neither by the fund nor by its distributor.

However, the solicitation of non-regulated qualified investors (mainly independent asset managers, pension funds, family office and companies managing their treasury) is now subject to the following requirements :

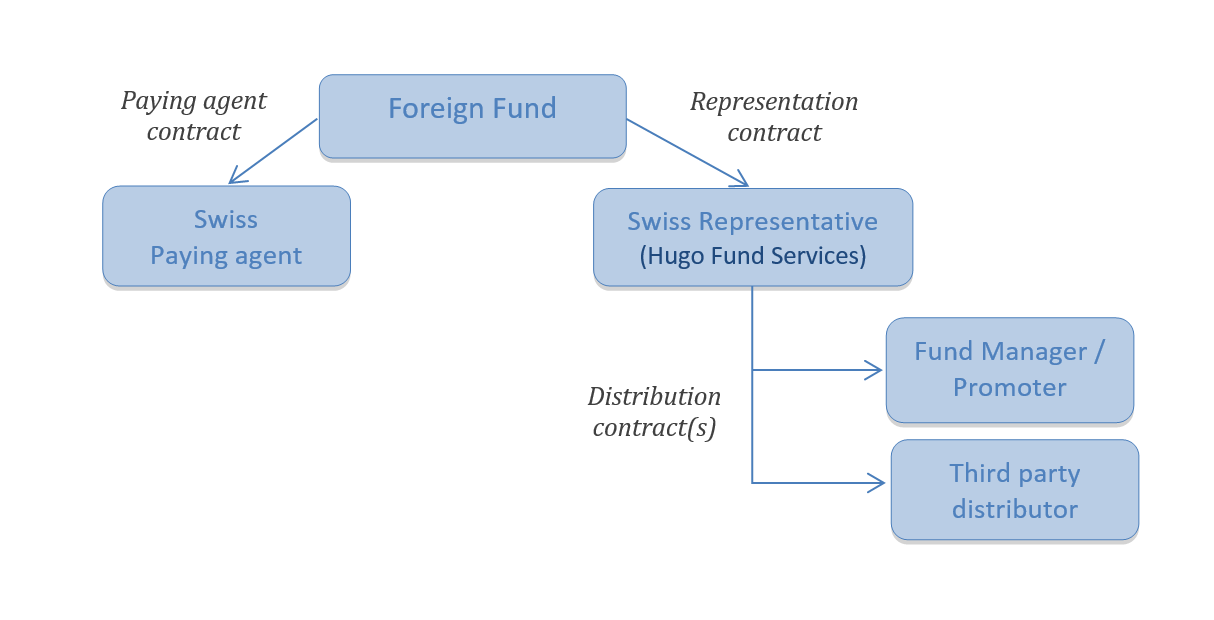

- The fund provider must appoint a Swiss legal representative whose role is twofold : a) to be the permanent Swiss contact point and complaint bureau for investors in Switzerland and FINMA, and b) to organise and to a certain extent supervise the distribution in Switzerland by entering into a Swiss distribution agreement with the fund distributor

- The fund provider must appoint a Swiss paying agent, which must be a Swiss bank. The appointment is compulsory but the use of the paying agent for channelling subscription or redemption payments is at the discretionary option of the investor.

- The Swiss legal representative must enter into a distribution agreement with the distributor of the fund represented (the entity that will solicit qualified investors in Switzerland). The scope of this distribution agreement is limited to regulatory issues. It can co-exist with a separate distribution agreement between the fund provider and the distributor focused on business issues. The CISA makes it a compulsory requirement that such agreement can only be entered into by the representative with foreign distributors regulated in their home jurisdiction and admitted for the distribution of collective investment schemes (at least the one they manage).

- The fund provider must insert a Swiss section in the prospectus, the OM or the PPM of the fund represented. The information contained in this Swiss section has been made mandatory by various provisions of the CISA and CISO and various industry guidelines made minimal standard by FINMA.

This new system is illustrated in the diagram

After a grace period of two years, these requirements have become compulsory for all foreign funds on March 1st 2015.

- Experience feedback

Based on our experience (Hugo has so far entered into representation agreement for more than 400 funds) the Swiss requirements appear to be relatively light. For fund managers, the drain on human resources, time consumption and financial costs are very limited in comparison to the cost of implementing the AIFMD. A full “on-boarding” to allow compliant distribution in Switzerland to non-regulated qualified investors can take less than two weeks if diligently pursued and with a reasonable annual cost. Following a minimal set-up effort, few on-going adjustments to previous marketing habits, and a relatively low cost, business can move forward quite similarly to the previous private placement regime.

More than two years after the entry into force of the new regime and the on-boarding in Switzerland of probably over 2’000 foreign alternative funds, a number of practical issues and interpretations of the regulation have emerged. We discuss a number of these issues hereunder in the form of a Q&A.

- What exactly is the role of the legal representative?

The representative of foreign funds offered only to qualified investors has a dual role :

- The representative represents the fund vis-à-vis the Swiss-based investor and FINMA (Articles 123 to 125 CISA). The representative is the permanent contact point of the fund in Switzerland for qualified investors and FINMA avoiding them to chase the fund or the fund manager abroad if required. Vis-à-vis the qualified investors the representative also acts as a complaint office. These roles provide a genuine level of protection to Swiss-Based qualified investors.

- The representative organises the distribution of funds by entering into a Swiss distribution agreement (Art. 30a and 131 a CISO), providing the legal framework for distribution and to a certain extent supervises the distribution by checking the regulatory status of the distributors (Art 19 para. 1 bis CISA) as well as their compliance with the SFAMA provisions for distributors (checking organisation and obtaining the yearly written confirmation of the distributor).

Even though their starting point is the organisation of distribution in Switzerland, these two roles are distinct. To be properly performed, the first role needs continuity from the moment a Swiss-based investor invests in the foreign fund and lasting up to the moment the last Swiss-based investor redeems and is reimbursed by the fund. The second role can be discontinued when distribution stops. Terminating the distribution arrangements shall not affect the obligations derived from the first role.

- From which point in time is it compulsory for a fund provider to appoint a representative and paying agent?

The obligation to appoint a representative and paying agent is initially related to the distribution activities in/from Switzerland. Therefore, a foreign collective investment scheme needs to appoint both of them prior to starting distribution activities. The relevant activities in this regard are those set out in Art. 3 CISA in conjunction with Art. 3 CISO and FINMA Circular 2013/9 “Distribution of collective investment schemes”.

- Can pre-sales and pre-marketing activities also trigger a duty to appoint a representative and a paying agent?

“Pre-Sales” and “Pre-Marketing” activities are considered to be “distribution” if the fund marketed has been launched or if its key elements (investment policy, fee policy, main contracting parties such as custodian and management company) have been determined and are set forth for marketing purposes. Under such circumstances presales or premarketing can be considered as distribution even though the fund has not yet been legally formed or formally launched. This would typically be the case for closed-end funds marketed on the basis of a draft PPM and before closing of the LPA. But it may also be the case of an open-ended fund offered on the basis of a draft OM or term sheet.

By contrast, abstract discussions with potential investors not relating to a specific product are not deemed to have the nature of distribution. This is the case, for example, if information is provided on certain strategies or composites without reference being made to an actual specific product. Market testing should thus remain possible.

- Until which point in time do a representative and paying agent have to be appointed?

This issue is still debated by the industry participants.

For some, a difference must be made between open-ended and closed-ended funds. Open-ended funds should have a representative and a paying agent only as long as the fund is marketed in Switzerland. By contrast closed-end funds should keep a representative as long as investors based in Switzerland hold shares or interest in the fund.

For other industry participants, given the role of the representative as the permanent contact point of the fund in Switzerland for qualified investors and FINMA, there should be no difference between open and closed-end funds and all foreign funds offered or held by non-regulated qualified investors should maintain a representative as long as investors based in Switzerland hold shares or interest in the fund.

This latter solution appears to be the only one that does not create confusion and uncertainty.

- Is it compulsory to insert the text of the “Swiss section mandatory wording” in the Prospectus, OM or PPM?

The purpose of the mandatory wording is to provide Swiss based investors with certain pieces of information such as the name and address of the representative and paying agent, the place of performance and jurisdiction, the Swiss regulatory status of the fund and certain additional details concerning retrocessions and rebates. This information can either be inserted in the fund documents such as the prospectus, OM or PPM. It can also be provided under the form of a separate documents attached to the fund documents. It may even be disclosed under the form of a specific document addressed nominally to the investor. What is compulsory is that the investor based in Switzerland had access to the information and that such availability of the information can be proven by the distributor.

- The Swiss Qualified Investor Marketplace

The first wave of investment managers keen on being compliant day one and registering for representation was, for a large part, managers with an already active presence in Switzerland. Once the deadline passed other managers have more time to consider needs, to proceed with balancing costs and the ability to raise assets, as well as proceeding with a thorough analysis of each country’s regulatory framework.

As a Swiss representative, we are in a unique position to see the flows of funds marketing in Switzerland, or close to doing so. Representatives have numerous discussions with marketing teams, lawyers, third party marketing firms and placement agents. Hugo is a company with a thorough understanding of the alternative investment universe as partners and employees mostly are ex-allocators to alternative investment funds. Our market intelligence tells us that fund managers should not look away from Switzerland if trying to raise assets. Indeed, the landscape has changed, and investors may not be as easy to reach as in the past, requiring more effort to identify them and a longer sales process. There is however a continued level of interest with a steady flow of assets into alternative investment funds. The current regulatory framework in Switzerland, not limiting any type of fund structure to market to qualified investors, should increase comfort levels of professional investors in Switzerland to venture further into diverse strategies and structures.

Yves Hervieu-Causse

Email: [email protected]

Tel: +41 22 707 41 60

Yves Hervieu-Causse has 28 years of fund industry and global asset management experience. Before founding Hugo Fund Services in 2014, Yves was a founding partner in Aforge Finance Holding (now part of the Degroof banking group) and CEO of Aforge investment management business in Geneva and Paris. Prior to starting up Aforge, Yves spent over 12 years at Unigestion, a Geneva-based wealth management firm allocating client assets to hedge funds, private equity and long only funds, in multiple investment roles. A lawyer and economist by training, Yves has been admitted to the Geneva Bar (1984) is a graduate of the Graduate Institute of International Studies, Geneva (1980), the University of Geneva law school (1982) and New York University School of Law (1986).